One-Time Close New Construction

Overview

Priority 1 Lending offers One-Time Close New Construction for conventional and VA loans. This is an opportunity for our clients to generate new business as they continue to strengthen relationships with real estate agents, build new relationships with builders/contractors and further expand their portfolio of options for borrowers.

BENEFITS

- PRIORITY 1 LENDING is arming our partners to help more borrowers and first-time homebuyers make their first home or next home their dream home

- Builders don't have to pay for the construction upfront, then sell the home to a borrower. They can create the borrower's dream home and get a loan before construction even begins. Helping save time and money by only having to close once and covering one set of closing costs!

- PRIORITY 1 LENDING's process has a contractor approval component. Meaning we vet the contractor and obtain references to make sure they are credible. This helps give peace of mind to your borrower, that they have gone with a good option.

- Other lenders require intense documentation, high interest rates, and large down payments. PRIORITY 1 LENDING helps reduce the headaches, keep the project moving, create transparency and peace of mind for all parties involved, and offer the same great service on these loans, as we always do

- After the first approval the borrower is good to go, no need to reapprove them!

What is a One-Time Close New Construction loan?

- A One-Time Close New Construction loan is a single closing construction loan. The construction portion is short-term financing that is modified into permanent financing upon completion of the project. A single closing construction mortgage can be closed as a purchase or a refinance.

What is a single closing?

- A single closing construction loan is the combination of financing of the construction and the permanent mortgage. There is a single closing transaction that occurs prior to construction beginning.

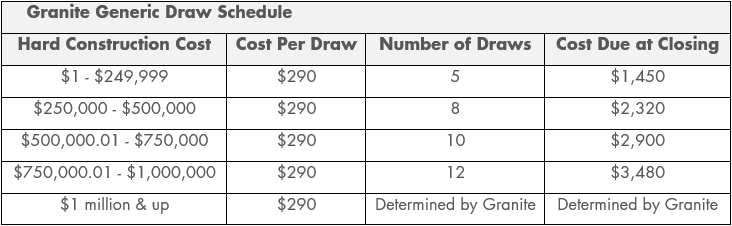

- Closing costs/fees that the borrower is responsible for are collected at closing. Funds are accessed through draws and there will be an initial draw at closing for proceeds to the contractor to begin the construction project.